The majority of Estonians do not regularly participate in financial planning, a trend evident in statistics showing the Estonian household savings rate plummeting from 13.7% to 0.2% between 2020 and 2022.

This decline highlights a significant gap in favorable conditions and legislation in Estonia to support individuals in cultivating lifelong saving habits, not just for retirement but also for managing shorter-term expenses.

Problem

Savings and pension planning alone are not effective enough to secure the financial health of the population. Notwithstanding pensions, Estonians also wish to save money for other major expenses such as purchasing property, renovations, education, hobbies and travel.

Although investment accounts are becoming increasingly popular, today, people with a higher level of financial literacy primarily make use of them. Meanwhile, tax exemptions do not apply to early withdrawals from Pillar II or III of the Estonian pension system.

Therefore, improving the financial health of the nation requires, in addition to pensions and savings options, also the possibility to conveniently invest in the medium-long term.

Solution

Grünfin, a company participating in Accelerate Estonia’s program, has proposed specific solutions to improve Estonia’s investment environment and increase motivation for long-term investment, involving employers in the process. Employers are excellent partners to make improvements in individuals’ financial literacy and behaviour with the greatest impact and scale possible. In order to engage employers, financial motivation must first be built.

One proposal is to extend the tax exemption for stock options to other investment products that are more broad-based and diversified. Since the risk level of the products would be similar to pension funds, it would also be suitable for a wider group of society.

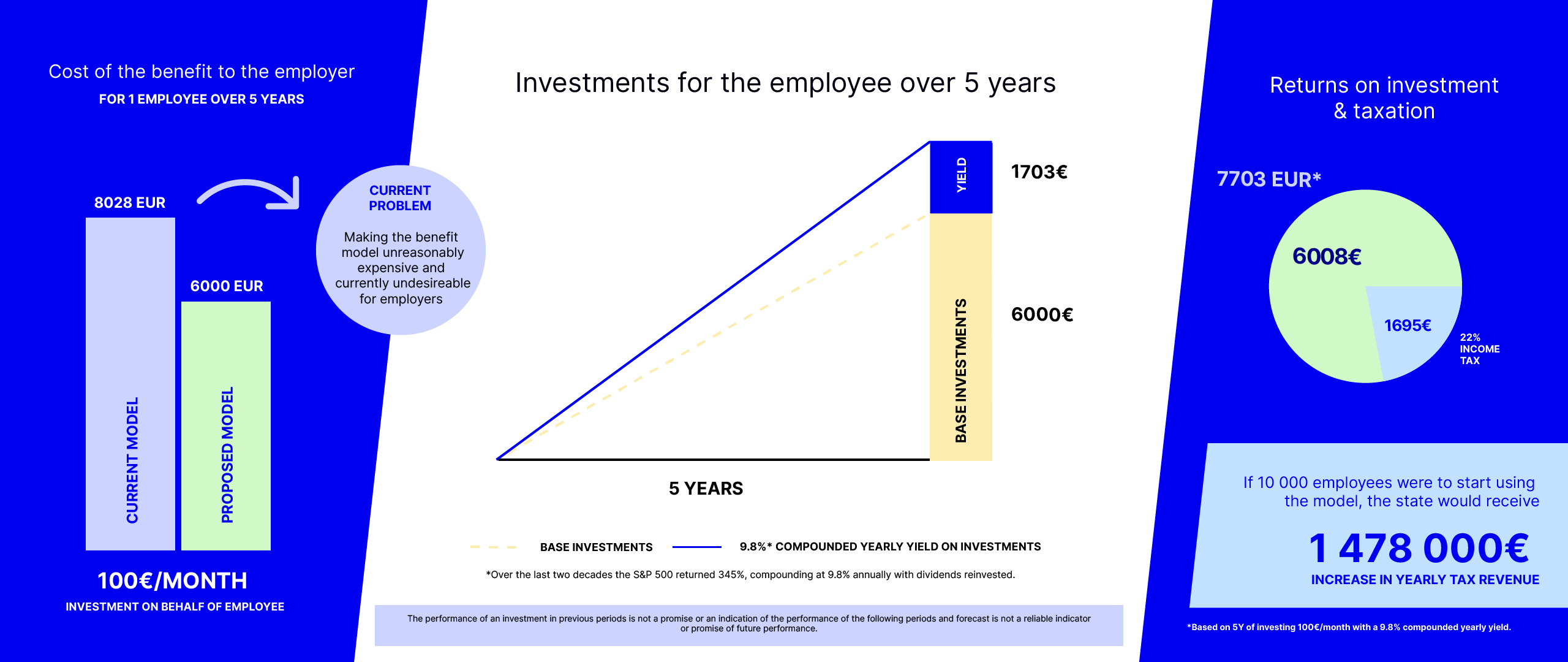

When looking at long-term investments, 51% of Estonians wish for their employers to contribute to their pension savings in place of salary increases. Likewise, this proposal creates a model whereby the employer makes investments for the employee and alongside the employee.

The solution would require the exemption of long-term (for example, more than 3 years) savings programs from fringe benefits tax and taxing them similarly to option programs, only with income tax. The tax exemption applies if the employer makes an investment on behalf of the employee, in addition to their salary. Since the employer’s investment is an additional benefit that would otherwise not exist, it also establishes a new tax revenue base for the state.

This approach creates a new opportunity by enabling convenient and automatic investments, particularly benefiting those with lower financial literacy, limited knowledge, and a lack of confidence to start investing independently.

End goal

Grünfin and Accelerate Estonia believe that the proposed legislative changes would significantly increase the number of people actively engaged in long-term investing. This, in turn, would enhance the overall financial well-being of the population, improve financial knowledge and investment skills, and potentially reduce social inequality and economic pressures.

Following the implementation of this change in law Grünfin will develop a pilot product, which, after successful testing and validation at the national level in Estonia, will make it easier to adapt to the wider sector and possibly also export the solution to other countries.

Furthermore, the proposed regulatory change would create a new market segment in the investment landscape. As a result of the tax exemption, employers have a greater motivation to invest on behalf of their employees and hence do not only inject new capital to the market but also to the state budget in the form of income tax.

During the cooperation, Accelerate Estonia involves the necessary parties and conducts an impact analysis of the given solution on people’s financial behaviour and the economy.

Results

The employer investment solution proposed by Grünfin as part of the Accelerate Estonia program reached its conclusion at the end of 2024. Although the project did not evolve into a functioning service, it enabled a comprehensive impact analysis, which mapped the needs of both employees and employers.

In summary, the impact analysis showed that if Grünfin’s solution and the corresponding legislation were thoughtfully designed, it would be possible to create a service that benefits both employee and employers alike with the state also benefitting. It would increased financial literacy, savings rates, and investment activity among the population, while also contributing to the development of a new financial services market. Furthermore, over a 10-year period, the investment package could bring an additional €5 to €7 millioninto thestate budget.

There is clear interest in implementing an employer-based investment package. 60% of employees who participated in the survey would be interested in employer-provided investments, and 74% would contribute additional funds themselves. This is seen as a way to improve financial security, especially considering that 43% of Estonia’s working-age population rates their material well-being as rather poor or very poor.

Employers also see potential in the solution – 76% of employers participating in the survey would consider implementing it in their company. However, the most important motivating factor for them is the availability of a tax incentive. Without it, their interest is low.

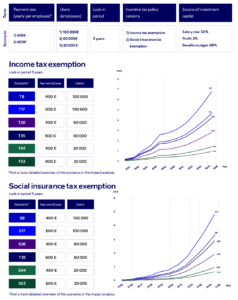

Accordingly, one of the goals of the impact analysis was to map out possible scenarios for applying tax incentives and assess their effects. It was found that if the incentive is reasonably limited, there are two implementation models where not only the employer and employee benefit, but the state also sees a positive return.

Under the current tax regulation, employer interest in the solution is low, which is why the solution has not been adopted and has therefore not had a societal impact. However, the insights gained from the analysis and Grünfin’s experience have left behind a valuable knowledge base, which can certainly be used as a foundation in future legislative developments.

The full impact analysis is available in Estonian and can be read here, and a summary of the findings in English can be read here.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.